Lab 3 - R Code#

Group 3: Valerie Dube, Erzo Garay, Juan Marcos Guerrero y Matías Villalba,

1. Neyman Orthogonality Proof#

\(Y_{nx1}=\alpha D_{nx1}+W_{nxp}\beta_{px1}+\epsilon_{nx1}\\ \widetilde{Y}_{nx1}=Y_{nx1}-W_{nxp}X_{{{Yw}_{px1}}}\\ \widetilde{D}_{nx1}=D_{nx1}-W_{nxp}X_{{{Dw}_{px1}}}\\ W=Matrix\ composed\ by\ one\ variable\ in\ each\ column\\ X=Vector\ of\ coefficients\\ n=N° observations\\ p=N° confounders \\\ \\\ \\\ M(a,\eta)=E[(\widetilde{Y}_{nx1}(\eta_{1})-a\widetilde{D}(\eta_{2})_{nx1})'(\widetilde{D}(\eta_{2})_{nx1})]=0\\ \frac{\partial a}{\partial \eta}=-[\frac{\partial M}{\partial a}(\alpha,\eta_{0})]^{-1}[\frac{\partial M}{\partial \eta}(\alpha,\eta_{0})]\\ \frac{\partial M}{\partial \eta}(\alpha,\eta_{0})=\frac{\partial M}{\partial \eta_{1}}(\alpha,X_{Yw},X_{Dw})+\frac{\partial M}{\partial \eta_{2}}(\alpha,X_{Yw},X_{Dw})\\ S_{1}=\frac{\partial M}{\partial \eta_{1}}(\alpha,X_{Yw},X_{Dw}) , S_{2}=\frac{\partial M}{\partial \eta_{2}}(\alpha,X_{Yw},X_{Dw})\)

Demonstration 1:#

\(Given\ the\ general\ formula\,\ before\ using\ (\alpha,X_{Yw},X_{Dw}): \widetilde{Y}_{nx1}=Y_{nx1}-W_{nxp}\eta_{{{1}_{px1}}} ,\ \widetilde{D}_{nx1}=D_{nx1}-W_{nxp}\eta_{{{2}_{px1}}}: \\\ \\\ S_{1}=\frac{\partial M}{\partial \eta_{1}}|_{(\alpha,W_{Yw},W_{Dw})}\\\ \\\ =\frac{\partial E[(\widetilde{Y}_{nx1}(\eta_{1})-a\widetilde{D}(\eta_{2})_{nx1})'(\widetilde{D}(\eta_{2})_{nx1})}{\partial \eta_{1}}|_{(\alpha,W_{Yw},W_{Dw})}=\frac{\partial E[Y_{nx1}-W_{nxp}\eta_{{{1}_{px1}}}-aD_{nx1}+aW_{nxp}\eta_{{{2}_{px1}}})'(D_{nx1}-W_{nxp}\eta_{{{2}_{px1}}})}{\partial \eta_{1}}|_{(\alpha,W_{Yw},W_{Dw})}\\\ \\\ Substituting\ (\alpha,W_{Yw},W_{Dw})\ in\ (a,\eta_{1},\eta_{2})\\\ \\\ =\frac{\partial E[(\widetilde{Y}_{nx1}(\eta_{1})-a\widetilde{D}(\eta_{2})_{nx1})'(\widetilde{D}(\eta_{2})_{nx1})]}{\partial \eta_{1}}|_{(\alpha,W_{Yw},W_{Dw})}=E[(W_{nxp})'(D_{nx1}-W_{n*p}\eta_{{2}_{px1}})]|_{(\alpha,W_{Yw},W_{Dw})}\\ =E[(W_{nxp})'(D_{nx1}-W_{n*p}X_{{{Dw}_{px1}}})]\\ =E[W'_{pxn}D_{nx1}-W'_{pxn}W_{nxp}(W'_{pxn}W_{nxp})^{-1}(W'_{pxn}D_{nx1})]\\ =E[W'_{pxn}D_{nx1}-I_{pxp}(W'_{pxn}D_{nx1})]=E[W'_{pxn}D_{nx1}-W'_{pxn}D_{nx1}]=E[0]\\ S_{1}=0\)

Demonstration 2:#

\(Given\ the\ general\ formula\,\ before\ using\ (\alpha,X_{Yw},X_{Dw}): \widetilde{Y}_{nx1}=y_{nx1}-W_{nxp}\eta_{{{1}_{px1}}} ,\ \widetilde{D}_{nx1}=D_{nx1}-W_{nxp}\eta_{{{2}_{px1}}}\\\ \\\ S_{2}=\frac{\partial M}{\partial \eta_{2}}|_{(\alpha,W_{Yw},W_{Dw})}=0\\\ \\ =\frac{\partial E[(\widetilde{Y}_{nx1}(\eta_{1})-a\widetilde{D}(\eta_{2})_{nx1})'(\widetilde{D}(\eta_{2})_{nx1})}{\partial \eta_{2}}|_{(\alpha,W_{Yw},W_{Dw})}=\frac{\partial E[Y_{nx1}-W_{nxp}\eta_{{{1}_{px1}}}-aD_{nx1}+aW_{nxp}\eta_{{{2}_{px1}}})'(D_{nx1}-W_{nxp}\eta_{{{2}_{px1}}})}{\partial \eta_{2}}|_{(\alpha,W_{Yw},W_{Dw})}\\ =\frac{\partial E[-Y_{1xn}'W_{nxp}\eta_{{2}_{px1}}+\eta'_{{1}_{1xn}}W'_{pxn}W_{pxn}\eta_{{2}_{px1}}+aD'_{1xn}W_{nxp}\eta_{{2}_{px1}}+a\eta'_{{2}_{1xp}}W'_{pxn}D_{nx1}-a\eta'_{{2}_{1xp}}W'_{pxn}W_{nxp}\eta_{{2}_{px1}}]}{\partial \eta_{2}}|_{(\alpha,W_{Yw},W_{Dw})}\\ =E[-W'_{pxn}Y_{nx1}+W'_{pxn}W_{nxp}\eta_{{1}_{px1}}+aW'_{pxn}D_{nx1}+aW'_{pxn}D_{nx1}-aW'_{pxn}W_{nxp}\eta_{{2}_{px1}}-aW'_{pxn}W_{nxp}\eta_{{2}_{px1}}]|_{(\alpha,W_{Yw},W_{Dw})}\\\ \\\ Substituting\ (\alpha,W_{Yw},W_{Dw})\ in\ (a,\eta_{1},\eta_{2})\\\ \\ =E[-W'_{pxn}Y_{nx1}+W'_{pxn}W_{nxp}X_{{{yw}_{px1}}}+\alpha W'_{pxn}D_{nx1}+\alpha W'_{pxn}D_{nx1}-\alpha W'_{pxn}W_{nxp}X_{{{Dw}_{px1}}}-\alpha W'_{pxn}W_{nxp}X_{{{Dw}_{px1}}}]\\ =E[-W'_{pxn}Y_{nx1}+W'_{pxn}W_{nxp}(W'_{pxn}W_{nxp})^{-1}(W'_{pxn}Y_{nx1})+\alpha W'_{pxn}D_{nx1}+\alpha W'_{pxn}D_{nx1}-\alpha W'_{pxn}W_{nxp}(W'_{pxn}W_{nxp})^{-1}(W'_{pxn}D_{nx1})-\alpha W'_{pxn}W_{nxp}(W'_{pxn}W_{nxp})^{-1}(W'_{pxn}D_{nx1})]\\ =E[-W'_{pxn}Y_{nx1}+-W'_{pxn}Y_{nx1}+\alpha W'_{pxn}D_{nx1}+\alpha W'_{pxn}D_{nx1}-\alpha W'_{pxn}D_{nx1}-\alpha W'_{pxn}D_{nx1}]=E[0]=0\\ S_{2}=0\)

2. Code Section#

2.1. Orthogonal Learning#

# Install and load necessary packages

#install.packages(c("glmnet", "parallel", "ggplot2", "gridExtra", "hdm", "cowplot"))

library(hdm)

library(glmnet)

library(parallel)

library(ggplot2)

library(gridExtra)

library(cowplot)

Loading required package: Matrix

Loaded glmnet 4.1-8

Simulation Design#

We are going to simulate 3 different trials to show the properties we talked about orthogonal learning.

For that we first define a function that runs a single observation of our simulation.

simulate_once <- function(seed) {

set.seed(seed)

n <- 100

p <- 100

beta <- 1 / (1:p)^2

gamma <- 1 / (1:p)^2

mean <- 0

sd <- 1

X <- matrix(rnorm(n * p, mean, sd), n, p)

D <- (X %*% gamma) + rnorm(n, mean, sd) / 4

Y <- 10 * D + (X %*% beta) + rnorm(n, mean, sd)

# Single selection method

r_lasso <- rlasso(Y ~ D + X, post = TRUE)

coef_matrix <- r_lasso$coefficients[-c(1, 2)]

SX_IDs <- which(coef_matrix != 0)

# In case all X coefficients are zero

if (length(SX_IDs) == 0) {

naive_model <- lm(Y ~ D)

naive_coef <- coef(summary(naive_model))[2, 1]

} else {

X_D <- cbind(D, X[, SX_IDs])

naive_model <- lm(Y ~ X_D)

naive_coef <- coef(summary(naive_model))[2, 1]

}

# Regress residuals

resY <- residuals(rlasso(Y ~ X, post = FALSE))

resD <- residuals(rlasso(D ~ X, post = FALSE))

orthogonal_model <- lm(resY ~ resD)

orthogonal_coef <- coef(summary(orthogonal_model))[2, 1]

return(c(naive_coef, orthogonal_coef))

}

Then we define a function that runs the simulation on its enterity, using parallel computing and the function we previously defined.

run_simulation <- function(B) {

cl <- makeCluster(detectCores()) # Create a cluster using all available cores

on.exit({

stopCluster(cl)

}, add = TRUE) # Ensure the cluster is stopped when the function exits, even if there's an error

clusterExport(cl, list("simulate_once", "rlasso", "coef", "residuals", "summary", "set.seed", "matrix", "rnorm", "cbind", "lm", "which")) # Export necessary objects and functions to the cluster

results <- tryCatch({

parLapply(cl, 1:B, simulate_once) # Run the simulation in parallel

}, error = function(e) {

message("Error during parallel execution: ", e)

stopCluster(cl)

stop(e)

})

Naive <- sapply(results, function(x) x[1])

Orthogonal <- sapply(results, function(x) x[2])

return(list(Naive = Naive, Orthogonal = Orthogonal))

}

Orto_breaks <- seq(8, 12, by = 0.2)

Naive_breaks <- seq(8, 12, by = 0.2)

Next we run the simulations with 100, 1000, and 10000 iterations and plot the histograms for the Naive and Orthogonal estimations

options(warn=-1)

Bs <- c(100, 1000, 10000)

custom_theme <- theme_classic() +

theme(

panel.background = element_blank(),

panel.border = element_rect(color = "black", fill = NA, linewidth = 1),

panel.grid.major = element_blank(),

panel.grid.minor = element_blank(),

plot.background = element_blank()

)

for (B in Bs) {

start_time <- Sys.time()

results <- run_simulation(B)

Naive <- results$Naive

Orthogonal <- results$Orthogonal

end_time <- Sys.time()

elapsed_time <- as.numeric(difftime(end_time, start_time, units = "secs"))

df1 <- data.frame(Orthogonal = Orthogonal)

df2 <- data.frame(Naive = Naive)

vlines_df <- data.frame(x = c(mean(df1$Orthogonal), 10),

label = c("Estimated Treatment Effect", "True Effect"))

p1 <- ggplot(df1, aes(x = Orthogonal)) +

geom_histogram(aes(y = after_stat(density)), breaks = Orto_breaks, fill = "lightblue", color = "NA") +

geom_density(color = "darkblue", linewidth=1) +

geom_vline(data = vlines_df, aes(xintercept = x, color = label, linetype = label), linewidth = 1) +

scale_x_continuous(limits = c(8, 12)) +

ggtitle("Orthogonal estimation") +

xlab("Estimated Treatment Effect")+

scale_color_manual(values = c("Estimated Treatment Effect" = "blue", "True Effect" = "red")) +

scale_linetype_manual(values = c("Estimated Treatment Effect" = "dashed", "True Effect" = "dashed")) +

custom_theme+

labs(color = "Legend", linetype = "Legend")+

theme(legend.direction = "horizontal")

p2 <- ggplot(df2, aes(x = Naive)) +

geom_histogram(aes(y = after_stat(density)), breaks = Naive_breaks, fill = "lightblue", color = "NA") +

geom_density(color = "darkblue", linewidth=1) +

geom_vline(aes(xintercept = mean(Naive)), color = "blue", linetype = "dashed", linewidth=1) +

geom_vline(xintercept = 10, color = "red", linetype = "dashed", linewidth=1) +

scale_x_continuous(limits = c(8, 12)) +

ggtitle("Naive estimation") +

xlab("Estimated Treatment Effect")+

custom_theme

# Extract the legend

legend <- suppressWarnings(get_legend(p1))

# Remove the legends from the individual plots

p1 <- p1 + theme(legend.position = "none")

p2 <- p2 + theme(legend.position = "none")

# Arrange the plots and the legend

combined_plot <- plot_grid(p1, p2, ncol = 2, align = "v")

combined_plot_with_legend <- plot_grid(combined_plot, legend, ncol = 1, rel_heights = c(1, 0.07))

grid.arrange(combined_plot_with_legend, ncol = 1, top = paste("Simulation with", B, "iterations"))

print(paste("Time taken for", B, "iteration simulation:", round(elapsed_time, 2), "seconds"))

}

[1] "Time taken for 100 iteration simulation: 4.61 seconds"

We can se that the orthogonal estimation yields on average a coeficient more centered on the true effect than the naive estimation. This method of estimation that utilizes the residuals of lasso regresion and helps reduce bias more efficiently than the naive estimation method. This is because it leverages the properties explained on the begining of this notebook rather than just controlling for a relevant set of covariates which may induce endogeneity.

We have used parallel computing because it is supposed to allow us to achieve better processing times. It can significantly lower the running time of computations due to its ability to distribute the workload across multiple processing units.

As an example, we can see how long it would have taken to run the simulation with 1000 iteration if we had not utilized parallel computing.

Without parallel computing

run_simulation <- function(B) {

Naive <- numeric(B)

Orthogonal <- numeric(B)

for (i in 1:B) {

results <- simulate_once(i)

Naive[i] <- results[1]

Orthogonal[i] <- results[2]

}

return(list(Naive = Naive, Orthogonal = Orthogonal))

}

start_time <- Sys.time()

results <- run_simulation(1000)

Naive <- results$Naive

Orthogonal <- results$Orthogonal

end_time <- Sys.time()

elapsed_time <- as.numeric(difftime(end_time, start_time, units = "secs"))

print(paste("Time taken for 1000 iteration simulation:", round(elapsed_time, 2), "seconds"))

[1] "Time taken for 1000 iteration simulation: 129.2 seconds"

We can see that if we were to not use parallel computing, the processing time would be higher. It took 129 seconds to achieve what we achieved in 27.

2.2. Double Lasso - Using School data#

# Install necessary packages

install.packages("tidyverse")

install.packages("lme4")

install.packages("stargazer")

install.packages("caTools")

install.packages("caret")

install.packages("glmnet")

Warning message:

"dependencies 'MASS', 'Matrix', 'lattice' are not available"also installing the dependencies 'fastmap', 'colorspace', 'sys', 'bit', 'ps', 'sass', 'cachem', 'nlme', 'farver', 'munsell', 'rappdirs', 'askpass', 'bit64', 'processx', 'highr', 'xfun', 'yaml', 'bslib', 'fontawesome', 'htmltools', 'tinytex', 'backports', 'ellipsis', 'glue', 'lifecycle', 'memoise', 'blob', 'tidyselect', 'vctrs', 'data.table', 'gtable', 'isoband', 'mgcv', 'scales', 'gargle', 'cellranger', 'curl', 'ids', 'rematch2', 'mime', 'openssl', 'timechange', 'fansi', 'utf8', 'systemfonts', 'textshaping', 'vroom', 'tzdb', 'progress', 'callr', 'fs', 'knitr', 'rmarkdown', 'selectr', 'stringi', 'broom', 'conflicted', 'cli', 'dbplyr', 'dplyr', 'dtplyr', 'forcats', 'ggplot2', 'googledrive', 'googlesheets4', 'haven', 'hms', 'httr', 'jsonlite', 'lubridate', 'magrittr', 'modelr', 'pillar', 'purrr', 'ragg', 'readr', 'readxl', 'reprex', 'rlang', 'rvest', 'stringr', 'tibble', 'tidyr', 'xml2'

Warning message:

"unable to access index for repository https://cran.r-project.org/bin/windows/contrib/3.6:

cannot open URL 'https://cran.r-project.org/bin/windows/contrib/3.6/PACKAGES'"Packages which are only available in source form, and may need

compilation of C/C++/Fortran: 'fastmap' 'colorspace' 'sys' 'bit' 'ps'

'sass' 'cachem' 'nlme' 'farver' 'rappdirs' 'askpass' 'bit64'

'processx' 'xfun' 'yaml' 'htmltools' 'backports' 'ellipsis' 'glue'

'tidyselect' 'vctrs' 'data.table' 'isoband' 'mgcv' 'scales' 'curl'

'mime' 'openssl' 'timechange' 'fansi' 'utf8' 'systemfonts'

'textshaping' 'vroom' 'tzdb' 'fs' 'stringi' 'cli' 'dplyr' 'haven'

'jsonlite' 'lubridate' 'magrittr' 'purrr' 'ragg' 'readr' 'readxl'

'rlang' 'tibble' 'tidyr' 'xml2'

These will not be installed

installing the source packages 'munsell', 'highr', 'bslib', 'fontawesome', 'tinytex', 'lifecycle', 'memoise', 'blob', 'gtable', 'gargle', 'cellranger', 'ids', 'rematch2', 'progress', 'callr', 'knitr', 'rmarkdown', 'selectr', 'broom', 'conflicted', 'dbplyr', 'dtplyr', 'forcats', 'ggplot2', 'googledrive', 'googlesheets4', 'hms', 'httr', 'modelr', 'pillar', 'reprex', 'rvest', 'stringr', 'tidyverse'

Warning message in install.packages("tidyverse"):

"installation of package 'munsell' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'highr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'fontawesome' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'tinytex' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'lifecycle' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'memoise' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'blob' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'cellranger' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'ids' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'rematch2' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'callr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'httr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'bslib' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'gtable' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'gargle' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'knitr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'conflicted' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'dtplyr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'forcats' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'hms' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'pillar' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'stringr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'progress' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'rmarkdown' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'selectr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'broom' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'dbplyr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'ggplot2' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'googledrive' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'googlesheets4' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'modelr' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'reprex' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'rvest' had non-zero exit status"Warning message in install.packages("tidyverse"):

"installation of package 'tidyverse' had non-zero exit status"Warning message:

"dependencies 'Matrix', 'MASS', 'lattice' are not available"also installing the dependencies 'utf8', 'pillar', 'vctrs', 'glue', 'fs', 'pkgbuild', 'diffobj', 'fansi', 'rematch2', 'tibble', 'brio', 'callr', 'cli', 'desc', 'digest', 'jsonlite', 'lifecycle', 'magrittr', 'pkgload', 'processx', 'ps', 'rlang', 'waldo', 'testthat', 'nlme', 'minqa', 'nloptr', 'RcppEigen'

Warning message:

"unable to access index for repository https://cran.r-project.org/bin/windows/contrib/3.6:

cannot open URL 'https://cran.r-project.org/bin/windows/contrib/3.6/PACKAGES'"Packages which are only available in source form, and may need

compilation of C/C++/Fortran: 'utf8' 'vctrs' 'glue' 'fs' 'diffobj'

'fansi' 'tibble' 'brio' 'cli' 'digest' 'jsonlite' 'magrittr'

'processx' 'ps' 'rlang' 'testthat' 'nlme' 'minqa' 'nloptr'

'RcppEigen' 'lme4'

These will not be installed

installing the source packages 'pillar', 'pkgbuild', 'rematch2', 'callr', 'desc', 'lifecycle', 'pkgload', 'waldo'

Warning message in install.packages("lme4"):

"installation of package 'rematch2' had non-zero exit status"Warning message in install.packages("lme4"):

"installation of package 'callr' had non-zero exit status"Warning message in install.packages("lme4"):

"installation of package 'desc' had non-zero exit status"Warning message in install.packages("lme4"):

"installation of package 'lifecycle' had non-zero exit status"Warning message in install.packages("lme4"):

"installation of package 'pillar' had non-zero exit status"Warning message in install.packages("lme4"):

"installation of package 'pkgbuild' had non-zero exit status"Warning message in install.packages("lme4"):

"installation of package 'waldo' had non-zero exit status"Warning message in install.packages("lme4"):

"installation of package 'pkgload' had non-zero exit status"Warning message:

"unable to access index for repository https://cran.r-project.org/bin/windows/contrib/3.6:

cannot open URL 'https://cran.r-project.org/bin/windows/contrib/3.6/PACKAGES'"installing the source package 'stargazer'

also installing the dependency 'bitops'

Warning message:

"unable to access index for repository https://cran.r-project.org/bin/windows/contrib/3.6:

cannot open URL 'https://cran.r-project.org/bin/windows/contrib/3.6/PACKAGES'"Packages which are only available in source form, and may need

compilation of C/C++/Fortran: 'bitops' 'caTools'

These will not be installed

Warning message:

"dependencies 'lattice', 'MASS', 'Matrix' are not available"also installing the dependencies 'parallelly', 'future', 'future.apply', 'colorspace', 'utf8', 'KernSmooth', 'lava', 'farver', 'munsell', 'fansi', 'pillar', 'tzdb', 'rpart', 'survival', 'nnet', 'prodlim', 'timechange', 'stringi', 'cli', 'glue', 'gtable', 'isoband', 'lifecycle', 'mgcv', 'rlang', 'scales', 'tibble', 'vctrs', 'class', 'proxy', 'data.table', 'dplyr', 'clock', 'ellipsis', 'gower', 'hardhat', 'ipred', 'lubridate', 'magrittr', 'purrr', 'tidyr', 'tidyselect', 'stringr', 'ggplot2', 'e1071', 'ModelMetrics', 'nlme', 'plyr', 'pROC', 'recipes', 'reshape2'

Warning message:

"unable to access index for repository https://cran.r-project.org/bin/windows/contrib/3.6:

cannot open URL 'https://cran.r-project.org/bin/windows/contrib/3.6/PACKAGES'"Packages which are only available in source form, and may need

compilation of C/C++/Fortran: 'parallelly' 'colorspace' 'utf8'

'KernSmooth' 'farver' 'fansi' 'tzdb' 'rpart' 'survival' 'nnet'

'prodlim' 'timechange' 'stringi' 'cli' 'glue' 'isoband' 'mgcv'

'rlang' 'scales' 'tibble' 'vctrs' 'class' 'proxy' 'data.table'

'dplyr' 'clock' 'ellipsis' 'gower' 'ipred' 'lubridate' 'magrittr'

'purrr' 'tidyr' 'tidyselect' 'e1071' 'ModelMetrics' 'nlme' 'plyr'

'pROC' 'reshape2' 'caret'

These will not be installed

installing the source packages 'future', 'future.apply', 'lava', 'munsell', 'pillar', 'gtable', 'lifecycle', 'hardhat', 'stringr', 'ggplot2', 'recipes'

Warning message in install.packages("caret"):

"installation of package 'future' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'munsell' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'lifecycle' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'hardhat' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'future.apply' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'pillar' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'gtable' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'stringr' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'recipes' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'lava' had non-zero exit status"Warning message in install.packages("caret"):

"installation of package 'ggplot2' had non-zero exit status"Warning message:

"dependency 'Matrix' is not available"also installing the dependencies 'survival', 'RcppEigen'

Warning message:

"unable to access index for repository https://cran.r-project.org/bin/windows/contrib/3.6:

cannot open URL 'https://cran.r-project.org/bin/windows/contrib/3.6/PACKAGES'"Packages which are only available in source form, and may need

compilation of C/C++/Fortran: 'survival' 'RcppEigen' 'glmnet'

These will not be installed

library(tidyverse)

library(lme4)

library(stargazer)

library(caTools)

library(caret)

library(glmnet)

library(rsample)

library(hdm)

Error in library(tidyverse): there is no package called 'tidyverse'

Traceback:

1. library(tidyverse)

df <- read.csv("./data/bruhn2016.csv")

first(df, 5)

| Row | outcome.test.score | treatment | school | is.female | mother.attended.secondary.school | father.attened.secondary.school | failed.at.least.one.school.year | family.receives.cash.transfer | has.computer.with.internet.at.home | is.unemployed | has.some.form.of.income | saves.money.for.future.purchases | intention.to.save.index | makes.list.of.expenses.every.month | negotiates.prices.or.payment.methods | financial.autonomy.index |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Float64 | Int64 | Int64 | String3 | String3 | String3 | String3 | String3 | String3 | String3 | String3 | String3 | String3 | String3 | String3 | String3 | |

| 1 | 47.3674 | 0 | 17018390 | NA | NA | NA | NA | NA | NA | 1 | 1 | 0 | 29 | 0 | 1 | 52 |

| 2 | 58.1768 | 1 | 33002614 | NA | NA | NA | NA | NA | NA | 0 | 0 | 0 | 41 | 0 | 0 | 27 |

| 3 | 56.6717 | 1 | 35002914 | 1 | 1 | 1 | 0 | 0 | 0 | 1 | 0 | 0 | 48 | 0 | 1 | 56 |

| 4 | 29.0794 | 0 | 35908915 | 1 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 42 | 0 | 0 | 27 |

| 5 | 49.5635 | 1 | 33047324 | 1 | 0 | 0 | 0 | 0 | 1 | 0 | 1 | 0 | 50 | 0 | 1 | 31 |

# Drop missing values

df <- df %>% drop_na()

df

Error in library(dplyr): there is no package called 'dplyr'

Traceback:

1. library(dplyr)

missing_count = sum(ismissing, eachcol(df))

0

# Define the vector of dependent variable names

dependent_vars <- c("outcome.test.score", "intention.to.save.index", "negotiates.prices.or.payment.methods", "has.some.form.of.income", "makes.list.of.expenses.every.month", "financial.autonomy.index", "saves.money.for.future.purchases", "is.unemployed")

["outcome.test.score", "treatment", "school", "is.female", "mother.attended.secondary.school", "father.attened.secondary.school", "failed.at.least.one.school.year", "family.receives.cash.transfer", "has.computer.with.internet.at.home", "is.unemployed", "has.some.form.of.income", "saves.money.for.future.purchases", "intention.to.save.index", "makes.list.of.expenses.every.month", "negotiates.prices.or.payment.methods", "financial.autonomy.index"]

# Define an array of dependent variable names

ddependent_vars <- c("outcome.test.score",

"intention.to.save.index",

"negotiates.prices.or.payment.methods",

"has.some.form.of.income",

"makes.list.of.expenses.every.month",

"financial.autonomy.index",

"saves.money.for.future.purchases",

"is.unemployed")

8-element Vector{String}:

"outcome.test.score"

"intention.to.save.index"

"negotiates.prices.or.payment.methods"

"has.some.form.of.income"

"makes.list.of.expenses.every.month"

"financial.autonomy.index"

"saves.money.for.future.purchases"

"is.unemployed"

For Lasso regressions, we split the data into train and test data, and standarize the covariates matrix

X <- df[, !(names(df) %in% dependent_vars)]

y <- df[, (names(df) %in% dependent_vars)]

set.seed(42)

# Split the data into training and testing sets

trainIndex <- createDataPartition(y[,1], p = 0.8, list = FALSE)

X_train <- X[trainIndex, ]

X_test <- X[-trainIndex, ]

y_train <- y[trainIndex, ]

y_test <- y[-trainIndex, ]

# Extract 'treatment' and remove it from 'X_train' and 'X_test'

T_train <- X_train$treatment

T_test <- X_test$treatment

X_train <- X_train[, !names(X_train) %in% "treatment"]

X_test <- X_test[, !names(X_test) %in% "treatment"]

# Standardize the covariates matrix

scale <- preProcess(X_train, method = c("center", "scale"))

X_train_scaled <- predict(scale, X_train)

X_test_scaled <- predict(scale, X_test)

# Combine the scaled training and testing data

X_scaled <- rbind(X_train_scaled, X_test_scaled) %>%

arrange(rownames(.))

# Combine the treatment training and testing data

T <- rbind(T_train, T_test) %>%

arrange(rownames(.))

2.2.2. Regressions#

a. OLS#

From 1 - 3 regression: measures treatment impact on student financial proficiency

From 4 - 6 regression: measures treatment impact on student savings behavior and attitudes

From 7 - 9 regression: measures treatment impact on student money management behavior and attitudes

From 10 - 12 regression: measures treatment impact on student entrepreneurship and work outcomes

# OLS regressions with "Student Financial Proficiency" as dependent variable

ols_score_1 <- lm(outcome.test.score ~ treatment, data = df)

ols_score_2 <- lm(outcome.test.score ~ treatment + school + failed.at.least.one.school.year, data = df)

ols_score_3 <- lm(outcome.test.score ~ treatment + school + failed.at.least.one.school.year + is.female + mother.attended.secondary.school + father.attended.secondary.school + family.receives.cash.transfer + has.computer.with.internet.at.home, data = df)

# OLS regressions with "Intention to save index" as dependent variable

ols_saving_1 <- lm(intention.to.save.index ~ treatment, data = df)

ols_saving_2 <- lm(intention.to.save.index ~ treatment + school + failed.at.least.one.school.year, data = df)

ols_saving_3 <- lm(intention.to.save.index ~ treatment + school + failed.at.least.one.school.year + is.female + mother.attended.secondary.school + father.attended.secondary.school + family.receives.cash.transfer + has.computer.with.internet.at.home, data = df)

# OLS regressions with "Negotiates prices or payment methods" as dependent variable

ols_negotiates_1 <- lm(negotiates.prices.or.payment.methods ~ treatment, data = df)

ols_negotiates_2 <- lm(negotiates.prices.or.payment.methods ~ treatment + school + failed.at.least.one.school.year, data = df)

ols_negotiates_3 <- lm(negotiates.prices.or.payment.methods ~ treatment + school + failed.at.least.one.school.year + is.female + mother.attended.secondary.school + father.attended.secondary.school + family.receives.cash.transfer + has.computer.with.internet.at.home, data = df)

# OLS regressions with "Has some form of income" as dependent variable

ols_manage_1 <- lm(has.some.form.of.income ~ treatment, data = df)

ols_manage_2 <- lm(has.some.form.of.income ~ treatment + school + failed.at.least.one.school.year, data = df)

ols_manage_3 <- lm(has.some.form.of.income ~ treatment + school + failed.at.least.one.school.year + is.female + mother.attended.secondary.school + father.attended.secondary.school + family.receives.cash.transfer + has.computer.with.internet.at.home, data = df)

# Show parameters in table using stargazer

stargazer(ols_score_1, ols_score_2, ols_score_3, ols_saving_1, ols_saving_2, ols_saving_3, ols_negotiates_1, ols_negotiates_2, ols_negotiates_3, ols_manage_1, ols_manage_2, ols_manage_3, type = "text",

title = "Regression Results",

column.labels = c("Student Financial Proficiency", "Intention to save index", "Negotiates prices or payment methods", "Has some form of income"),

covariate.labels = c("Failed at least one school year", "Female", "Father attended secondary school", "Family receives cash transfer", "Has computer with internet at home"))

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

| Dependent var 1: Student Financial Proficiency | Dependent var 2: Intention to save index | Dependent var 3: Negotiates prices or payment methods | Dependent var 4: Has some form of income | |||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) | |

| Intercept | 57.591*** | 59.377*** | 57.013*** | 49.016*** | 46.725*** | 45.407*** | 0.763*** | 0.856*** | 0.901*** | 0.639*** | 0.534*** | 0.553*** |

| (0.187) | (0.556) | (0.583) | (0.240) | (0.728) | (0.767) | (0.006) | (0.017) | (0.018) | (0.006) | (0.019) | (0.020) | |

| Failed at least one school year | -7.218*** | -6.759*** | -3.614*** | -3.354*** | 0.024*** | 0.016* | 0.005 | 0.002 | ||||

| (0.288) | (0.289) | (0.377) | (0.380) | (0.009) | (0.009) | (0.010) | (0.010) | |||||

| Female | 2.836*** | 1.357*** | -0.066*** | -0.054*** | ||||||||

| (0.257) | (0.339) | (0.008) | (0.009) | |||||||||

| Q("mother.attended.secondary.school") | 1.826*** | 1.380*** | -0.016** | 0.036*** | ||||||||

| (0.257) | (0.338) | (0.008) | (0.009) | |||||||||

| school | 0.000 | -0.000 | 0.000*** | 0.000*** | -0.000*** | -0.000*** | 0.000*** | 0.000*** | ||||

| (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | (0.000) | |||||

| treatment | 4.216*** | 4.392*** | 4.307*** | -0.070 | -0.005 | -0.047 | 0.001 | 0.001 | 0.003 | 0.017** | 0.016* | 0.018** |

| (0.261) | (0.255) | (0.253) | (0.335) | (0.334) | (0.333) | (0.008) | (0.008) | (0.008) | (0.009) | (0.009) | (0.009) | |

| Observations | 12222 | 12222 | 12222 | 12222 | 12222 | 12222 | 12222 | 12222 | 12222 | 12222 | 12222 | 12222 |

| R2 | 0.021 | 0.069 | 0.081 | 0.000 | 0.009 | 0.012 | 0.000 | 0.004 | 0.010 | 0.000 | 0.003 | 0.008 |

| Adjusted R2 | 0.021 | 0.068 | 0.080 | -0.000 | 0.009 | 0.011 | -0.000 | 0.004 | 0.010 | 0.000 | 0.003 | 0.008 |

| Residual Std. Error | 14.432 (df=12220) | 14.076 (df=12218) | 13.986 (df=12216) | 18.506 (df=12220) | 18.421 (df=12218) | 18.400 (df=12216) | 0.425 (df=12220) | 0.424 (df=12218) | 0.423 (df=12216) | 0.478 (df=12220) | 0.477 (df=12218) | 0.476 (df=12216) |

| F Statistic | 260.547*** (df=1; 12220) | 300.463*** (df=3; 12218) | 214.786*** (df=5; 12216) | 0.043 (df=1; 12220) | 38.533*** (df=3; 12218) | 29.248*** (df=5; 12216) | 0.018 (df=1; 12220) | 16.352*** (df=3; 12218) | 24.653*** (df=5; 12216) | 3.843** (df=1; 12220) | 12.839*** (df=3; 12218) | 19.652*** (df=5; 12216) |

| Note: | *p<0.1; **p<0.05; ***p<0.01 | |||||||||||

b. Double Lasso using cross validation#

Dependent var 1: Student Financial Proficiency

Step 1: We ran Lasso regression of Y (student financial proficiency) on X, and T on X

#we need matix structure

X_matrix <- as.matrix(X_scaled)

y_vector <- y_train$outcome.test.score

T_vector <- as.numeric(T_train)

# Lasso regression of Y on X with cross-validation

lasso_CV_yX <- cv.glmnet(X_matrix, y_vector, alpha = 1, lambda = seq(0.0001, 0.5, by = 0.001), nfolds = 10, maxit = 5000)

best_lambda_yX <- lasso_CV_yX$lambda.min

print(sprintf("Best lambda for Y on X: %.4f", best_lambda_yX))

# Estimate Y predictions with all X

y_pred_yX <- predict(lasso_CV_yX, s = best_lambda_yX, newx = as.matrix(X_scaled))

---------------------------------------------------------------------------

NameError Traceback (most recent call last)

Cell In[4], line 2

1 # Estimate y predictions with all X

----> 2 y_pred_yX = lasso_CV_yX.predict(X_scaled)

NameError: name 'lasso_CV_yX' is not defined

lasso_CV_TX <- cv.glmnet(X_matrix, T_vector, alpha = 1, lambda = seq(0.0001, 0.5, by = 0.001), nfolds = 10, maxit = 5000)

best_lambda_TX <- lasso_CV_TX$lambda.min

print(sprintf("Best lambda for T on X: %.4f", best_lambda_TX))

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Mejor lambda: 0.0011

# Estimate T predictions with all X

y_pred_TX <- predict(lasso_CV_TX, s = best_lambda_TX, newx = as.matrix(X_scaled))

Step 2: Obtain the resulting residuals

#y_pred_yX <- as.numeric(y_pred_yX)

#y_pred_TX <- as.numeric(y_pred_TX)

res_yX <- y$outcome.test.score - y_pred_yX

res_TX <- T - y_pred_TX

Step 3: We run the least squares of res_yX on res_TX

# Create a data frame for the residuals

residuals_data <- data.frame(res_yX = res_yX, res_TX = res_TX)

ols_score <- lm(res_yX ~ res_TX, data = residuals_data)

stargazer(ols_score, type = "text", title = "OLS Regression of Residuals")

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

| Dependent variable: res_yX | |

| (1) | |

| Intercept | 0.033 |

| (0.126) | |

| res_TX | 4.324*** |

| (0.253) | |

| Observations | 12222 |

| R2 | 0.023 |

| Adjusted R2 | 0.023 |

| Residual Std. Error | 13.945 (df=12220) |

| F Statistic | 292.956*** (df=1; 12220) |

| Note: | *p<0.1; **p<0.05; ***p<0.01 |

c. Double Lasso using theoretical lambda#

# Load necessary libraries

library(hdm)

# Define the RLasso class

RLasso <- setRefClass("RLasso",

fields = list(post = "logical"),

methods = list(

initialize = function(post = TRUE) {

.self$post <- post

},

fit = function(X, y) {

fit <- rlasso(X, y, post = .self$post)

.self$rlasso_ <- fit

return(.self)

},

predict = function(X) {

predictions <- predict(.self$rlasso_, newx = X)

return(as.matrix(X) %*% predictions$coefficients[-1] + predictions$coefficients[1])

},

nsel = function() {

sum(abs(coef(.self$rlasso_)[-1]) > 0)

}

)

)

lasso_model <- function() {

RLasso$new(post = FALSE)

}

model <- lasso_model()

model$fit(X, y)

y_pred <- model$predict(X)

Step 1:

# Assuming X_scaled, y, and T are prepared as in Python

# Estimate y predictions with all X

model_yX <- lasso_model()

model_yX$fit(X_scaled, y$outcome.test.score)

y_pred_yX <- model_yX$predict(X_scaled)

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

# Estimate T predictions with all X

model_TX <- lasso_model()

model_TX$fit(X_scaled, T)

y_pred_TX <- model_TX$predict(X_scaled)

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

Step 2:

res_yX <- y$outcome.test.score - y_pred_yX

res_TX <- T - y_pred_TX

Step 3:

library(lmtest)

library(sandwich)

library(stargazer)

df <- data.frame(res_yX, res_TX)

lasso_hdm_score <- lm(res_yX ~ res_TX, data = df)

summary(lasso_hdm_score)

# Display the regression table using stargazer

stargazer(lasso_hdm_score, type = "text")

Intel MKL WARNING: Support of Intel(R) Streaming SIMD Extensions 4.2 (Intel(R) SSE4.2) enabled only processors has been deprecated. Intel oneAPI Math Kernel Library 2025.0 will require Intel(R) Advanced Vector Extensions (Intel(R) AVX) instructions.

| Dependent variable: res_yX | |

| (1) | |

| Intercept | 0.000 |

| (0.126) | |

| res_TX | 4.316*** |

| (0.253) | |

| Observations | 12222 |

| R2 | 0.023 |

| Adjusted R2 | 0.023 |

| Residual Std. Error | 13.953 (df=12220) |

| F Statistic | 291.837*** (df=1; 12220) |

| Note: | *p<0.1; **p<0.05; ***p<0.01 |

# Save the ITT beta and the confidence intervals

beta_DL_theo <- coef(lasso_hdm_score)['res_TX']

conf_int_DL_theo <- confint(lasso_hdm_score, 'res_TX')

d. Double Lasso using partialling out method#

rlassoEffect = hdmpy.rlassoEffect(X_scaled, y['outcome.test.score'], T, method='partialling out')

rlassoEffect

beta_part_out = rlassoEffect['coefficient']

critical_value = 1.96 # For 95% confidence level

conf_int_part_out = [beta_part_out - critical_value * rlassoEffect['se'],

beta_part_out + critical_value * rlassoEffect['se']]

---------------------------------------------------------------------------

NameError Traceback (most recent call last)

Cell In[1], line 1

----> 1 rlassoEffect = hdmpy.rlassoEffect(X_scaled, y['outcome.test.score'], T, method='partialling out')

NameError: name 'hdmpy' is not defined

rlassoEffect <- rlassoEffect(x = X_scaled, y = y$outcome.test.score, d = T, method = "partiallingOut")

{'alpha': 4.313441,

'se': array([0.25271166]),

't': array([17.06862565]),

'pval': array([2.54111627e-65]),

'coefficients': 4.313441,

'coefficient': 4.313441,

'coefficients_reg': 0

(Intercept) 59.769260

x0 0.000000

x1 1.511205

x2 0.529423

x3 0.461196

x4 -2.878027

x5 -0.857569

x6 0.000000,

'selection_index': array([[False],

[ True],

[ True],

[ True],

[ True],

[ True],

[False]]),

'residuals': {'epsilon': array([[-10.04200277],

[-31.30841071],

[-15.13769394],

...,

[-17.22383794],

[ -3.93047339],

[ -4.88461742]]),

'v': array([[ 0.48682705],

[-0.513173 ],

[ 0.48682705],

...,

[ 0.48682705],

[-0.513173 ],

[-0.513173 ]], dtype=float32)},

'samplesize': 12222}

print(rlassoEffect)

critical_value <- 1.96

conf_int_part_out <- c(beta_part_out - critical_value * summary(rlassoEffect)$se,

beta_part_out + critical_value * summary(rlassoEffect)$se)

print(conf_int_part_out)

Results#

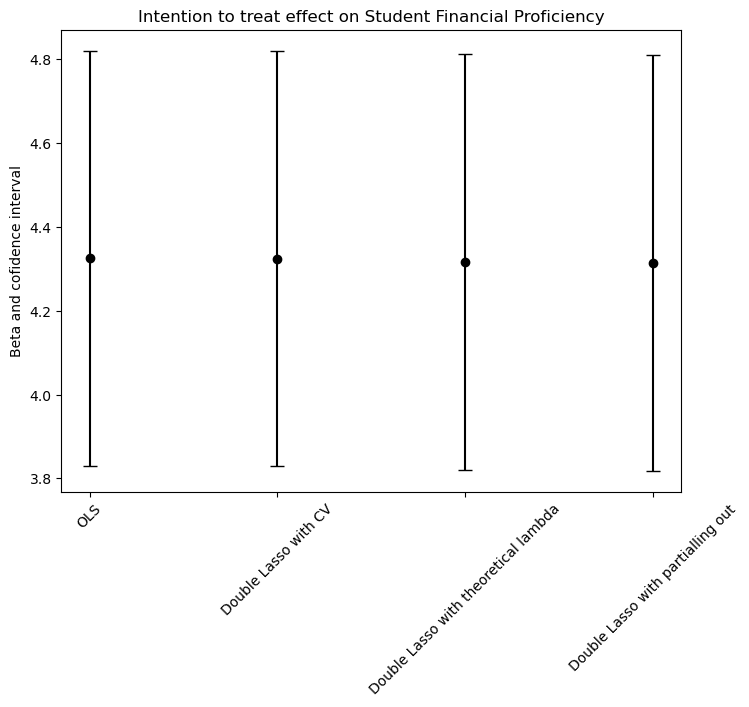

We found that the intention to treat effect (ITT) is very similar estimating with all 4 models (aproximately 4.3, with 95% of confidence). This could be because the ratio between the parameters and the number of observations p/n is small (8/12222 = 0.00065455735). In other words, we are not dealing with high dimensional data and the models from b. to d. will outperform the OLS when we are in the opposite scenario. In conclusion, we can say that the OLS model estimates the ITT just as good as the other models.

library(ggplot2)

data <- data.frame(

Model = c("OLS", "Double Lasso with CV", "Double Lasso with theoretical lambda", "Double Lasso with partialling out"),

Estimate = c(beta_OLS, beta_DL_CV, beta_DL_theo, beta_part_out),

Lower_CI = c(conf_int_OLS[1], conf_int_DL_CV[1], conf_int_DL_theo[1], conf_int_part_out[1]),

Upper_CI = c(conf_int_OLS[2], conf_int_DL_CV[2], conf_int_DL_theo[2], conf_int_part_out[2])

)

# Calculate the error sizes as required for geom_errorbar

data$ymin <- data$Estimate - data$Lower_CI

data$ymax <- data$Upper_CI - data$Estimate

# Create the plot

ggplot(data, aes(x = Model, y = Estimate, ymin = ymin, ymax = ymax)) +

geom_point() +

geom_errorbar(width = 0.2, size = 1, color = "black", position = position_dodge(0.05)) +

labs(title = "Intention to Treat Effect on Student Financial Proficiency",

y = "Beta and Confidence Interval") +

theme_minimal() +

theme(axis.text.x = element_text(angle = 45, hjust = 1))

ggsave("ITT_Effect_Size_Plot.png", width = 8, height = 6, units = "in")